“Inside the Bank” is a series revealing the secrets to creating and maintaining good banking relationships, written by bankers for the cannabis industry.

After years of working with cannabis businesses as banking executives, we’ve noticed a pattern. A frustrated cannabis operator calls. Maybe their account was just closed, or maybe they’re struggling to get approved in the first place. When we dig into what happened, the issue is almost never the nature of their cash-heavy business or the industry in which they operate. It’s how they run the company.

- Banks do not see cash volume itself as the main problem for cannabis businesses.

- They look for disciplined controls, daily reconciliations, deposit consistency, and clear documentation.

- Unpredictable deposits, weak internal controls, and poor communication can put banking relationships at risk.

- Operators who act “bank-ready” make long-term banking access more likely.

Cannabis operators often treat cash as just another piece of the machine: revenue to count, deposit, and move. From a bank’s perspective, however, cash provides a window into how disciplined, transparent, and predictable an operator’s internal controls are.

Why cash handling shapes banking risk

Cash is not the problem. Dealing in physical currency is an unavoidable reality in the cannabis industry. What matters to financial institutions is how that cash is handled, documented, and reconciled.

Higher volumes of physical currency increase the burden placed on the financial institution servicing the account. Banks must monitor the movement of funds under strict Bank Secrecy Act and anti-money-laundering obligations. They must also account for physical security exposure, insurance and custody risk, audit intensity, and regulatory scrutiny tied to every dollar that flows through a client’s business.

Institutions look closely at the predictability and structure of an operator’s cash practices. More cash on the premises means more work for everyone: more monitoring, more insurance exposure, more scrutiny when examiners come through. And none of it matters if you can’t show where the money came from.

When operators maintain clear controls and consistent deposit practices, they reduce operational and regulatory strain for the bank. Banks don’t evaluate businesses based on how much cash they generate. They evaluate discipline, documentation, and control.

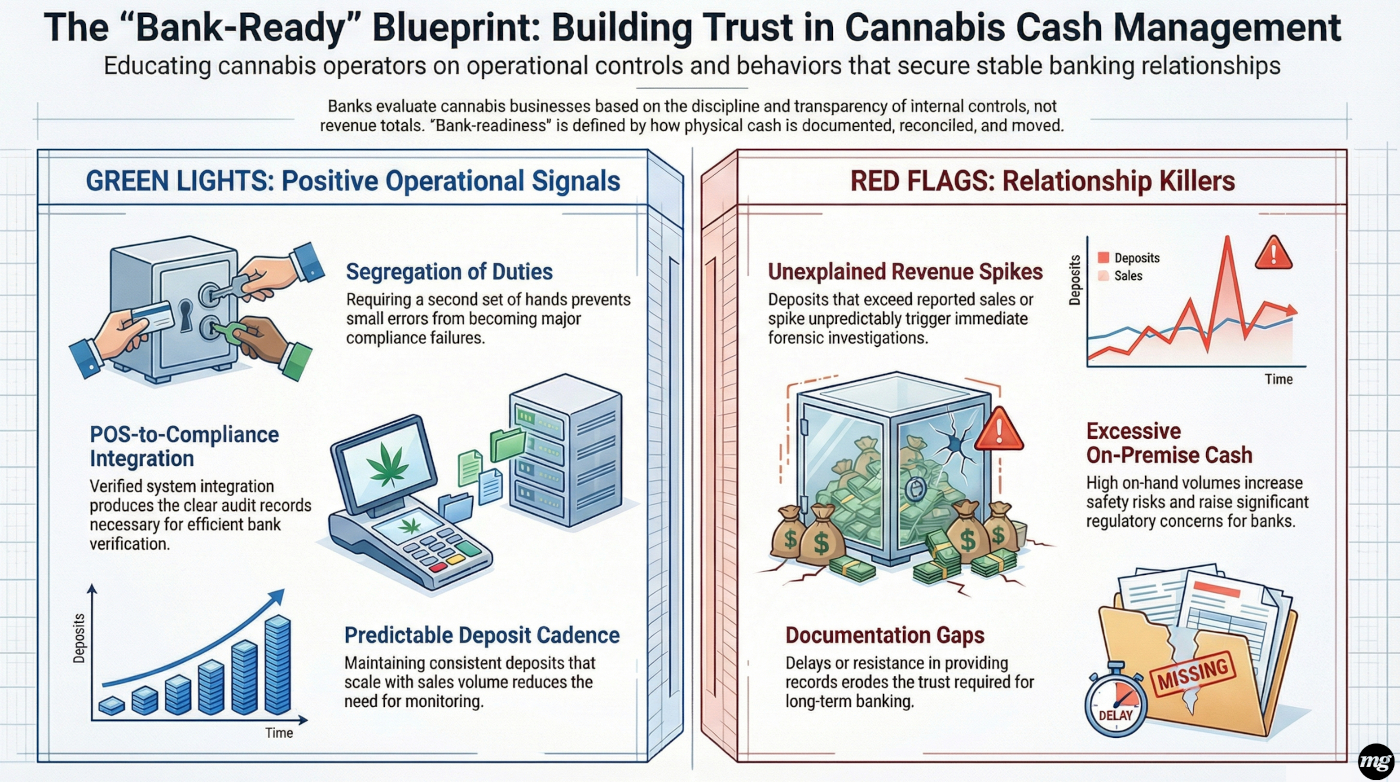

What do banks look for in a cannabis business?

Financial institutions serving cannabis businesses evaluate more than revenue totals. They watch how cash moves through an organization and whether those movements follow consistent, documented processes. Certain operational signals help determine whether a company is managing cash in a way that supports a stable banking relationship. Operators who minimize cash risk often signal they are minimizing regulatory risk as well.

Here’s what banks typically look for:

Written policies and procedures for handling cash

Documentation should detail counting, packaging, reconciling, and recording steps. Standard instructions include drawer closure, deposit preparation, variance logs, and role assignment for each step.

Segregation of duties across cash-handling roles

One person shouldn’t own the entire process. When a second set of hands is involved, small problems surface before they become something bigger.

Clear daily reconciliations between POS records and physical cash

Daily checks between transactions recorded at the point of sale (POS) and cash balances help verify accuracy. All differences should be logged and examined regularly.

Regular armored transport aligned with sales volume

Predictable pickup schedules signal operational discipline. When deposits follow a consistent cadence relative to revenue, banks can more easily reconcile account activity with reported sales.

Secure storage practices

Commercial-grade safes with restricted access demonstrate operators are treating cash as a controlled asset rather than a routine operational byproduct.

Verified integration between POS and compliance systems

System integration produces a clearer audit record and allows banks to confirm sales and deposit information more efficiently.

Deposits consistently align with recorded sales over time

Clean deposit-to-sales alignment gives banks confidence that internal reporting systems are accurate and reliable.

Predictability builds confidence

Deposit cadence should scale with sales velocity. The higher the volume, the shorter the cycle. Consistent deposits aligned with sales activity help banks understand how cash moves through the business and reduce the need for investigative monitoring.

Why do cannabis bank accounts get closed?

Conversely, certain patterns raise concern, and experienced cannabis bankers notice them right away.

Deposits that spike unpredictably or exceed reported sales

When deposits differ from recorded revenue, financial institutions investigate whether the cause is an error, a process issue, or missing documentation.

Excessive cash stored on premises

High on-hand cash amounts increase both safety and compliance concerns, particularly when deposit timing lacks an operational explanation.

Manual uploads or disconnected systems

Independent sales and compliance systems make it harder to confirm transaction data reflects actual operations.

Resistance to providing documentation

Delays or gaps in documentation make it harder for banks to verify the origin and movement of funds.

Casual approaches to internal controls

Irregular reconciliation steps, missing variance documentation, or ambiguous cash-handling roles aren’t minor housekeeping issues. They’re the kind of things that end banking relationships.

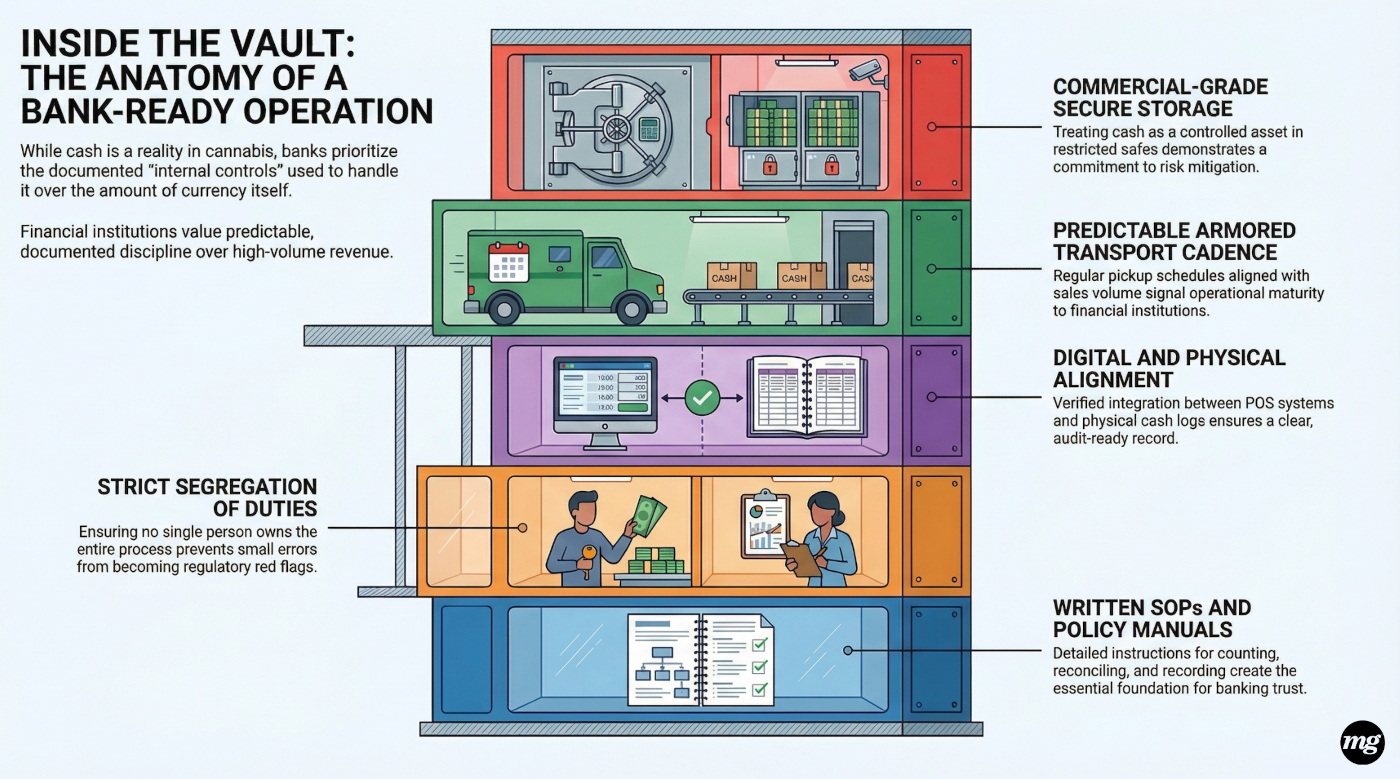

What makes a cannabis operator bank-ready?

Becoming “bank-ready” does not require complex systems, but it does require operational discipline. Institutions evaluate companies based on documented processes, consistent cash handling, and transparent responsibility for financial operations.

Key operational controls typically include:

Written policies and standard operating procedures

Documentation covers counting, packaging, reconciling, and recording. No single person should be able to move cash through the process unchecked. A second set of hands at the right moments keeps small errors from becoming serious ones.

Reconciliation and reporting

A daily comparison between recorded sales, physical cash, and bank deposits keeps the numbers consistent. If something is off, variance logs create a record of how the issue was investigated and resolved.

Transport and storage

Armored transport should follow a predictable schedule tied to sales velocity. Cash storage should be limited to secure, commercial-grade safes with restricted access. Internal loading of ATMs generally is discouraged; many institutions prefer cash-in-transit providers manage these transfers.

Documentation

If cash touched it, there should be a record of it. That means standard operating procedures, cash logs, reconciliations, chain-of-custody documentation, transport agreements, investor paperwork, and an explanation on file for any time deposits jumped.

Consistent documentation and predictable processes help reduce institutional risk and support stable banking relationships. Operators that integrate these practices into daily routines show banks they have the operational discipline that makes a long-term relationship possible.

How weak cash controls create bigger problems

Weak cash controls have a way of spreading. What starts as a banking issue rarely stays one.

When procedures are loose, telling the difference between an honest mistake and something worse becomes difficult. That ambiguity is exactly what regulators and forensic auditors are trained to find and once they’re looking, the burden falls on the operator to prove everything was clean. That’s an expensive, time-consuming position to be in, and it’s almost always avoidable.

There’s also a staff dimension that doesn’t get talked about enough. During every shift, dispensary employees handle significant amounts of cash. When that cash sits on-site longer than it should, the people responsible for it become uneasy. That’s not a compliance issue. It’s a morale issue, and it has a cost.

Why communication matters as much as controls

From a banker’s perspective, the single fastest way to damage a relationship is to let your bank find out about something before you tell them. Ownership change, new license, regulatory inquiry, a revenue jump that looks unusual. If that surfaces in monitoring data before you’ve picked up the phone, trust quickly erodes. In cannabis banking specifically, trust is hard to rebuild.

The cannabis operators who stay banked long-term aren’t necessarily running the most sophisticated operations. They’re just the ones who communicate before there’s a problem, document before they’re asked, and treat their bank more like a compliance partner than a necessary inconvenience. That posture makes everything easier — audits, renewals, and relationship conversations — because there’s nothing to explain away.

Stability beyond the balance sheet

For cannabis operators, careful cash management is a foundation for stable banking relationships and long-term operational resilience.

One piece of advice that gets shared often with operators: Run the business as if federal legalization will never arrive. Build controls strong enough to withstand regulatory scrutiny, forensic review, and financial stress. If your processes can hold up under that level of examination, your banking relationship is far more likely to endure.

The businesses that earn long-term banking access aren’t the ones with the cleanest balance sheets. They’re the ones banks never have to wonder about.

Cannabis Banking Questions, Answered

What do banks look for in a cannabis business?

Banks look for documented cash-handling procedures, segregation of duties, daily reconciliations, predictable deposit schedules, secure storage, and records that align deposits with reported sales.

What makes a cannabis operator bank-ready?

A bank-ready operator has written procedures, consistent reconciliations, secure cash storage, reliable transport practices, and documentation that explains how money moves through the business.

Why do cannabis bank accounts get closed?

Accounts are often disrupted not because the business handles cash, but because controls are weak, deposits are inconsistent, documentation is incomplete, or the bank is surprised by changes or anomalies.

Zach Michael Wright is a business development officer at Affinity Federal Credit Union, where he leads cannabis banking initiatives across New Jersey, New York, and Connecticut. He works directly with licensed operators to navigate complex regulatory frameworks, focusing on compliance, cash management, and risk mitigation within the evolving cannabis industry. His work centers on creating practical, compliant banking solutions that support both institutional requirements and operator realities. Wright also serves as board chair for the Housing and Redevelopment Commission for the City of New Brunswick, New Jersey.

As vice president of banking and financial services at Green Check, Stacy Litke regularly advises banks, regulators, and cannabis operators on how to move from “trying to get banked” to building relationships that last. Drawing on decades of experience across community banking, fintech, and consulting, she translates complex regulatory expectations and evolving market conditions into clear, executable practices. She has worked with more than 130 financial institutions to stand up and refine cannabis banking programs under intense regulatory scrutiny. Prior to Green Check, she served as senior vice president of operations for MountainOne, a $900-million institution in Massachusetts, and as managing director for Northeastern Banking Services Group.